Entering the credit market without a plan is like entering a high-stakes casino blindfolded. Most individuals think of loans as an emergency safety net or a fast track to buying the things they desire today.

But banks see your loan as an asset that will provide stable income for years to come.

To win this game, you have to turn yourself from a passive consumer to a smart financial planner. And understanding loans is essential.

This ultimate manual reveals the secrets of modern lending.

We are going to deconstruct the secret mechanics of borrowing, examine actionable tactics for optimising your credit footprint, and look at the exact tools you need to lock in the lowest cost of capital.

How Do Interest Rates Work

In essence, an interest rate is the premium you pay for the privilege of using someone else money.

Lenders do not lend money because they are generous people; they lend money expecting a return to compensate them for inflation. Also, the expense of running the business, and the chance that you may not pay them back.

To see how this plays out in your day-to-day existence, imagine two distinct borrowers:

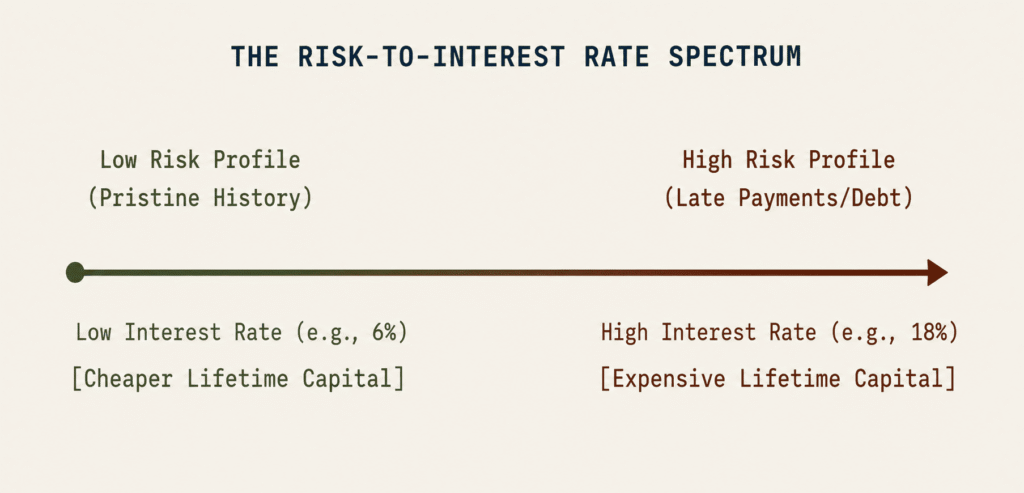

- Borrower A (High Risk) has a history of late payments and maxed-out credit cards.

- Borrower B (modest Risk): has a multi-year, clean history of paying on time and modest debt.

If both individuals are applying for a loan, what is the fundamental structure of how interest rates work? differs widely depending on their risk profile. Lenders face a sliding scale of risk.

Borrower A is statistically more likely to default, so the bank charges them a high interest rate (say 18%) to recover their principal as rapidly as feasible. Borrower B is a safe bet and, therefore, is rewarded with a low prime rate (say 6%).

There are two financial choices here; all you need to do is find the best one.

Moreover, interest rates can be set in two different ways:

1. Fixed Interest Rates:

The percentage is set in stone for the whole duration of your loan. If you sign a mortgage at 6.5% for 30 years, your payment will never change.

So you will have complete budget predictability regardless of what happens to the economy.

2.Variable/floating interest rates:

The rate is indexed to an underlying economic benchmark (such as the prime rate or SOFR).

If inflation heats up and the central bank pushes up its benchmark rates, your loan’s interest rate will immediately jump, instantly adding to your monthly burden.

What is the difference between unsecured and secured loans?

So you go to a bank and ask for money. Their underwriting department instantly starts figuring out how they can protect themselves if you fall on hard times. This structural safeguard creates two distinct domains in the lending market.

Secured loans are backed by collateral, while unsecured loans are not. It is essential in managing your individual liability and safeguarding your assets.

1. Secured Loans (Use Your Assets)

Secured loans are directly linked to a physical piece of collateral that you own or are buying.

If you fail to make your payments, the lender can legally repossess that asset to recover their losses without having to sue you.

Real-world example: A typical auto loan or home mortgage loan. If you buy a $40,000 truck and you miss your first three payments, the repo truck is going to be pulling up in your driveway to take the vehicle away.

The Benefit: Since the bank is taking on relatively little risk, they offer much lower interest rates and far bigger borrowing limits. Well, secured loans are safe, but understanding loans is still vital to mitigate long-term losses.

2. Unsecured Loans (Lending on Trust)

An unsecured loan does not require collateral. The bank lends you money based only on your financial character, the stability of your income, and your historical credit performance.

Real-life example: Credit cards, personal signature loans, and school loans. If you get a personal unsecured loan for a backyard remodel and miss payments, the bank cannot come and dig up your patio.

But they can sell your debt to a collection agency or sue you in civil court.

The Benefit: You can protect your personal property from repossession right now. But since the bank is assuming a huge risk, the interest rates are much higher, and the approval procedures are much stricter.

The Pre-App Launchpad: Building Credit Before You Apply for a Loan

Taking out a big loan with a bad credit score is a very expensive mistake. A low credit score might cost you an extra $50,000 to $100,000 in excess interest charges over the life of a house or business loan.

The best wealth-protection technique is to learn how to develop credit before you apply for a loan. Think of your credit score as your financial CV. You want it to look great before you go in for the interview.

Tactical Credit Building Roadmap

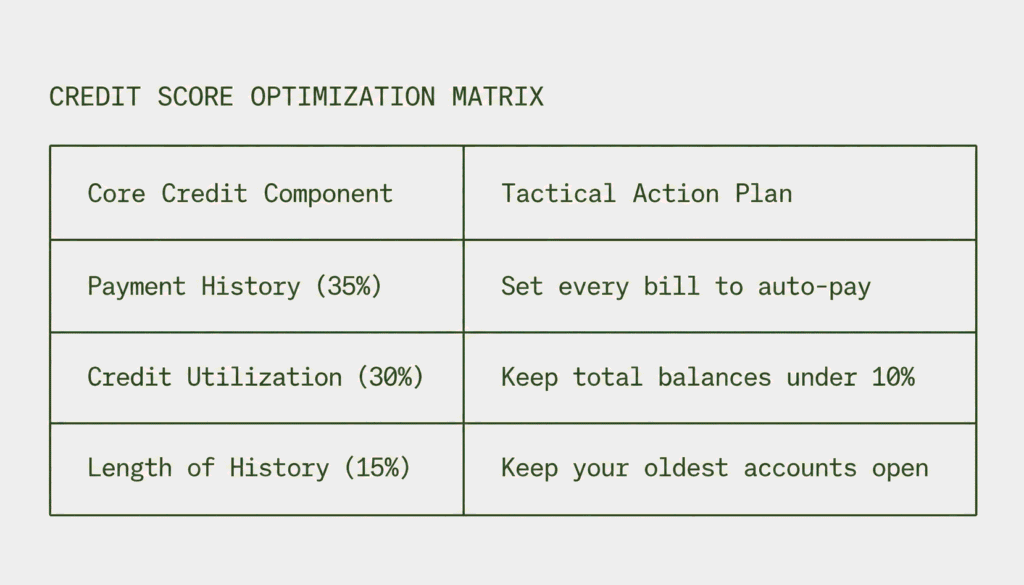

- Understand Credit Utilisation Ratio: Using your entire credit limit at once is your credit usage. If your credit card limit is $10,000, never exceed $1,000 in bills. Keeping your utilisation below 10% shows bureaus you can handle leverage without desperation.

- Secured Credit Card: Regular banks may deny credit card applicants without credit histories. A secured card requires a $500 cash deposit and a $500 credit limit. Pay one utility bill with this card each month and pay it off within 48 hours to boost your score safely.

- Authorised user status: Ask a family member with flawless credit and a long credit card history to be an authorised user. Your credit file shows decades of perfect payments. Instant algorithm boost.

How to Apply for a Personal Loan in 2026

Those days of printing out stacks of paper tax returns, scheduling physical visits, and sitting awkwardly in a bank cubicle are long gone. All of these things are unnecessary.

The entirety of the credit market has transitioned to digital channels that are both quick and secure.

Whenever you are prepared to initiate your borrowing strategy, you can submit an application for a personal loan online with complete assurance from your mobile device or laptop in a matter of minutes.

The Online Digital Application Checklist

You should put together the following digital documents in advance in order to guarantee that your online application will be accepted without any problems through the automated underwriting processes:

- A clean scan of your driver’s license or passport for the purpose of identification verification is an example of government-issued identification.

- The most recent two pay stubs, W-2 paperwork, or 1099 statements from independent contractors are all acceptable forms of proof of income.

- Please submit your most recent federal tax returns if you are self-employed or the owner of a small business to the Internal Revenue Service.

- In order for the lender to verify your bank account, they will need your routing and checking account numbers. This will allow them to safely deposit the funds directly into your account through an ACH transfer.

- For the purpose of verifying your identity, evaluating your debt-to-income ratios, and reviewing your credit records, online lending organisations use sophisticated algorithms once you have submitted your application.

Within sixty seconds, the majority of today’s systems are able to make a decision regarding an official approval, and within twenty-four to forty-eight hours, the cash will be sent back into your bank account.

Conclusion: Manage Your Finances

Loans are powerful financial tools. It can boost your long-term net worth if used carefully to pay off high-interest credit card debt or invest in an appreciating asset.

Mismanaged loans can quickly become costly anchors that drag down your lifestyle. Knowing interest rate math and debt structure.

By improving and understanding loans your credit before applying, you regain influence from institutional lenders.

You have to compare prices, do the calculations, and only borrow what improves your long-term freedom. And hence, Making Good Financial Choices.

FAQs

- Will a debt consolidation personal loan hurt my credit?Initially, but not long. A hard credit inquiry, which lowers your score temporarily, may occur when you apply for a new loan. However, the best debt consolidation personal loans can boost your credit score over time. By paying off many revolving credit card bills with your new loan installment, you immediately lower your credit utilisation ratio, which accounts for 30% of your credit score.

- May I repay my online personal loan early? Is there punishment?Many of the top digital lenders no longer levy prepayment fees, depending on their terms. Check for prepayment fees or exit penalties when searching online for personal loan interest rates. If your lender lets you pay off the loan early without penalty, any excess money goes to the principal, saving you a lot in interest.

- What is the minimum credit score for online personal loan applications?Specialized lenders exist for every credit tier, but competitive, low-interest unsecured personal loans require a score of 670 or higher. You can apply for a personal loan online with a score between 580 and 660, but the lender may charge a higher interest rate to cover their risk. If your score is below 580, seek a secured personal loan, which requires collateral.

- Is a debt consolidation loan the same as debt settlement?No, these are separate financial programs. A debt consolidation loan lets you take out a new loan at a lower interest rate to pay off your old creditors on time, protecting and improving your credit. Debt settlement involves intentionally halting payments, letting accounts go into delinquency, then negotiating with creditors to pay less than you owe. Debt settlement might damage your credit for seven years.

- After combining debt, what happens to my old credit cards?Your credit card accounts are active unless you call the bank to close them and have no balances. Keeping those accounts open with no balance is usually best for your credit score. Keep them open to retain your credit limit and average credit history. If holding open, empty cards is too much psychological temptation to overspend and build new debt with your new loan, closing them is best for your long-term financial health.