Debt is one of the most divisive subjects in personal finance. If mismanaged, it can become an unmanageable emotional albatross, limiting your life options and draining your financial worth.

But with a little forethought, leverage may be transformed from a problem into a high-powered asset.

Successful navigation of the consumer credit market requires a high level of financial awareness and precise instruments.

Hence, once you apply a proactive framework of Smart Loan Planning, you can efficiently optimise your liabilities, minimise your capital borrowing costs, and build a solid base of Increase Financial Security for you and your family.

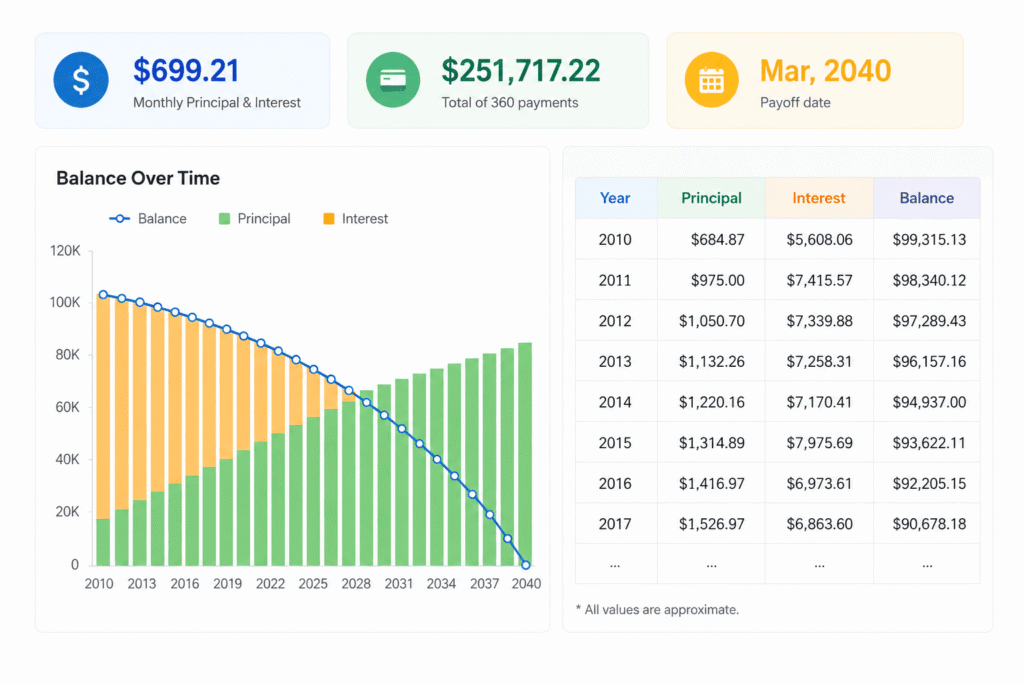

The Math Behind It: What Is Loan Amortisation?

To get a handle on consumer debt, you need to go beyond the plain dollar amount of the monthly payment and grasp the mathematical engine that drives it.

Amortisation is the systematic process of paying off a loan in regular installments over a certain length of time.

Each time you make a payment to your lender, that payment gets divided into two fully separate functional parts:

- The Interest Portion: The premium cost the bank keeps all for itself as profit for lending you the money.

- The Principal Portion: The actual money that goes to pay down the main mountain of debt you owe.

As you can see from the amortisation chart above, the ratio between these two parts changes over time. The first phase of your loan is when your remaining principal balance is at its greatest.

Interest is charged on the remaining big debt, so a lot of your early payments go towards interest.

Real World Example:

Say you borrow $30,000 for 5 years at an 8% interest rate. Your set monthly payment is exactly $608.29.

But in Month 1, a staggering $200 goes directly to interest, leaving only $408.29 to reduce the principal balance to $29,591.71.

By month 45, the remaining principal is much lower, thus the monthly interest charge lowers to about $60, allowing over $548 of the same monthly payment to aggressively chip away at the raw debt.

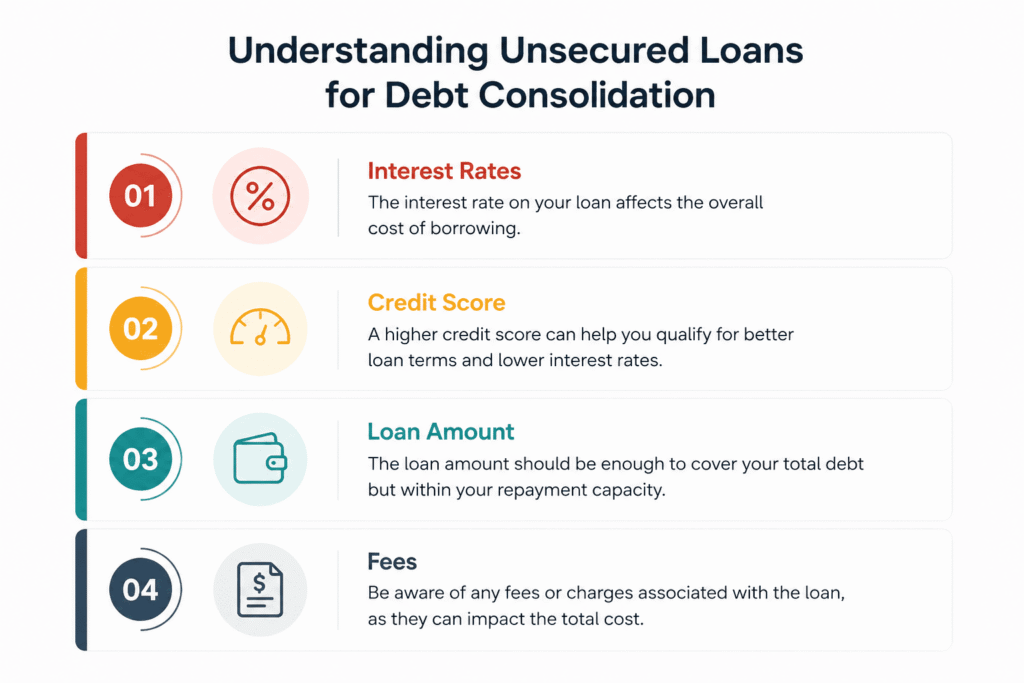

Secured vs. Unsecured Debt: What’s the Difference Between Collateral and Credit?

At the core of funders are risk mitigation companies. When they look at your application, they are primarily concerned with risk mitigation. They separated their lending products to protect their capital.

Understanding the difference between secured and unsecured debt is important for protecting your individual loans, assets, and growing your household cash flow responsibly.

1. Secured Debt (Collateralised by Real Assets)

Secured financing means you have to pledge a specific and valuable asset as financial collateral. In the event of unforeseen financial trouble, should you default on your obligations, the lender has the legal authority to seize the asset immediately in order to recover their financial losses.

More common variants: Residential mortgages, home equity lines of credit (HELOCs), and standard vehicle loans.

The strategic benefit: Because the physical asset reduces the bank’s capital risk, they’ll be willing to provide you access to much greater borrowing limits and much cheaper interest rates.

2. Debt without security (supported by financial character)

Unsecured finance is not backed by any physical collateral. The bank lends you capital based purely on your demonstrable income sources, debt-to-income ratios, and prior credit repayment performance.

Standard Common Variants: credit cards, medical financing arrangements, and personal loans.

Strategic Benefit: Your home, car, and liquid resources are legally shielded from quick foreclosure or repossession when you suddenly lose income. However, unsecured choices have substantially higher interest rates and fewer borrowing limits, as the bank assumes maximum risk.

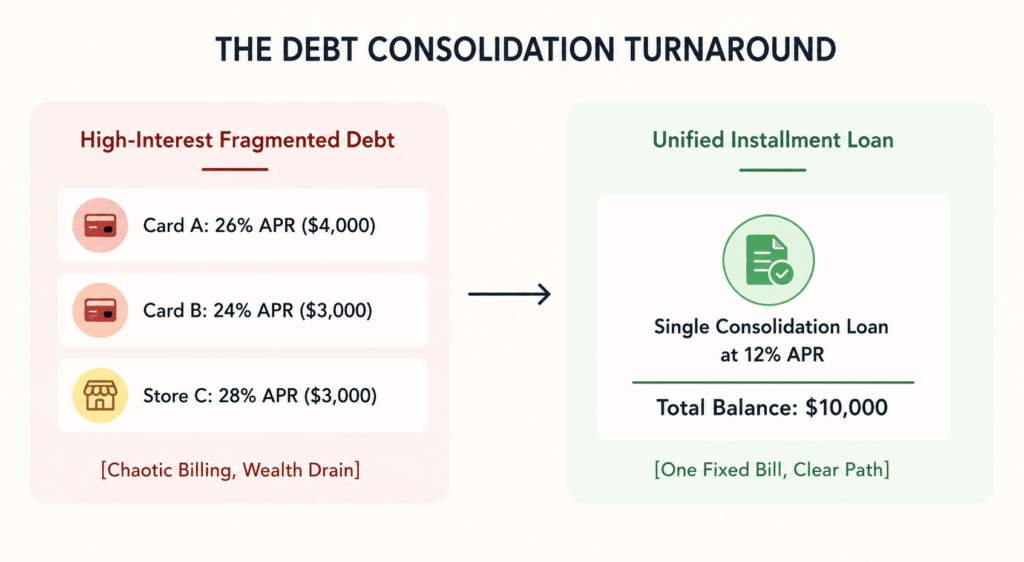

Best Debt Consolidation Loans for Bad Credit: Regaining Control

Small balances across a few high-interest credit cards or retail accounts are a major wealth destroyer.

Multiple due dates mean your monthly cash flow is split, and compound interest costs consume much of your hard-earned money.

If you have a scarred credit history, choosing the best debt consolidation loans for bad credit is an active offensive plan to break free from this expensive cycle.

If you want the greatest bad-credit consolidation solutions, look for lenders that focus on this specific niche and offer direct creditor payback options.

This means that the new lender will pay your credit card companies directly with the proceeds of the loan.

This approach ensures that you do not blow the lump amount payout inadvertently and locks in your lower interest rate structure immediately.

The Shopping Strategy: Shop Around For Personal Loan Rates

Do not settle for the first financing plan that comes your way. Lenders adjust their marketing algorithms to target the consumer who today values quickness over long-term savings.

To practise Smart Loan Planning, you need to slow down the timetable and actively research personal loan interest rates across different lending sites.

| Lender Institution Type | Average APR Range | Ideal For | Structural Underwriting Focus |

| Traditional National Banks | 6.5% – 12.0% | Prime credit profiles | Long-term existing banking relationships |

| Online Digital FinTech Platforms | 7.0% – 36.0% | Fast digital turnarounds | Alternate metrics (e.g., career paths) |

| Local Credit Unions | 5.0% – 10.5% | Value-conscious borrowers | community members and manual reviews |

But even a small 1.5% difference in your permitted APR might cost you thousands of dollars in total borrowing charges over your lifetime.

Always ask for a full loan estimate sheet and check the APR ( Annual Percentage Rate ) instead of the base rate.

The APR does appropriately capture hidden origination fees, processing administrative costs, and closing costs.

Get Personal Loan Pre-Approval Today

Here are the effective tips of getting a personal finances.

- There is no danger involved: When you get pre-approved, it’s based on a “soft credit check.” So you may see what your possible interest rates, loan amounts, and monthly payments might be without affecting your credit score one bit.

- Eliminates guesswork: Rather than crossing your fingers and praying a bank would accept you, pre-approval offers you concrete, hard statistics. You’ll know exactly what you qualify for before you waste time filling out a full application.

- The process is ridiculously fast: You don’t have to go to a bank branch or wait in an embarrassing interview. Most secure online lenders have turned this into a simple 2-3 minute digital form you can fill out from your couch.

- It provides you with wiggle room to browse around: Think of pre-approval like shopping with a quote in your palm. You can compare rates from two or three different lenders, set them side by side, and make them fight for your business.

- First, get these easy items together: You do not need to have much to keep things smooth. Just have your basic facts ready, your expected yearly income, your social security number (for the soft identity check), and an approximate sense of how much you need to borrow.

- Be aware of the fine print: Once you receive your pre-approval offers, pay attention to the APR (which includes hidden origination fees) and not simply the base interest rate. Also, confirm that the lenders you’re looking at don’t levy prepayment penalties for paying the loan off early.

Conclusion: Taking Charge of Your Financial Future

Leverage is an economic instrument, and like any tool, it is neutral; its worth depends on who uses it.

By understanding the mechanics of amortisation schedules, aligning the appropriate loan structures with your own goals, and using online pre-approvals for shopping around, you regain control from traditional banking institutions. You will surely make smart loan planning.

Also, you have to turn every liability into a conscious business investment decision, cut interest waste, and employ intelligent credit techniques to create a long-term strategy, and it will bring financial security.

FAQs

- Will a pre-approval ding my credit score?No, it does not The traditional pre-approval services will use a soft credit inquiry to determine your basic underwriting risk profile. This soft pull allows you to shop for personalised rates, terms, and payment alternatives safely without impacting your score or leaving a footprint on your credit record. You won’t be subject to that harsh inquiry until you actually pick an offer and allow the lender to complete the underwriting procedure.

- Can I pay extra principal to speed up the amortisation schedule?Yes, for most personal loans. Paying extra on your principal is one of the quickest methods to reduce the duration of your loan and maximise the amount of interest you save in the long run. But before you try this technique, check to see if your lender has any prepayment penalties. The best online personal loan lenders clearly say they don't have prepayment penalties, which means you can pay off your debt as soon as you desire.

- What is a good Debt-to-Income ratio for sensible loan planning?As a rule of thumb, maintain your debt-to-income (DTI) ratio below 35% to 40% to stay inside a healthy financial range. Your DTI ratio is all your required monthly debt payments ( mortgage, car loans, minimum credit card payments, personal loans ) divided by your gross monthly income. Lenders consider this number as an indicator of your likelihood of defaulting. Keeping this ratio low means you have lots of spare income for saving and investing.

- Is a secured loan better than an unsecured personal loan?Which one you choose relies on your risk tolerance and financial background. If your credit is perfect and you want to avoid putting your house or car on the line, an unsecured personal loan is generally your best option. However, if your credit history makes it impossible to qualify for fair conditions, a secured loan with a co-signer or security on the asset will help you qualify for a much better interest rate and save you thousands of dollars over the life of the loan.