Each time you deal with a bank, you are silently choosing what to do with your wealth. Traditional checking accounts lose value due to inflation, and monthly maintenance fees chip away at your savings.

To avoid the anxiety of living paycheck to paycheck, you need to be proactive about how you save, store, and use your money. You do not have to have a Wall Street pedigree to establish a solid economic base.

And by making deliberate, automated, and Smart Banking Decisions today, you can protect your household from economic shifts, outpace persistent inflation, and confidently chart a straightforward path to lasting Future Financial success.

If you are a Millennial, Gen Z professional, or a new investor who wants to optimize your personal finances, our guide is the perfect place to start.

What Are the Keys to Financial Success?

True financial capability rarely comes from risky stock market gambles or sudden economic windfalls.

This, rather, is built on a solid set of intentional, repeatable behaviors that protect and grow your cash flow over time.

The main keys to financial success are:

1. Guaranteed Liquidity:

Create a solid emergency cushion to protect yourself from sudden job loss or unexpected medical expenses without falling into high-interest credit card debt.

2. Automated Systems:

Eliminate human friction in your savings goals by setting aside a percentage of every paycheck to go directly into growth vehicles before you even have a chance to spend it.

3. Positive Arbitrage:

Steering clear of financial products that leech your wealth with high fees and low returns, and selecting platforms that increase your compound interest earnings.

Strategic Frameworks: How to make smart financial decisions

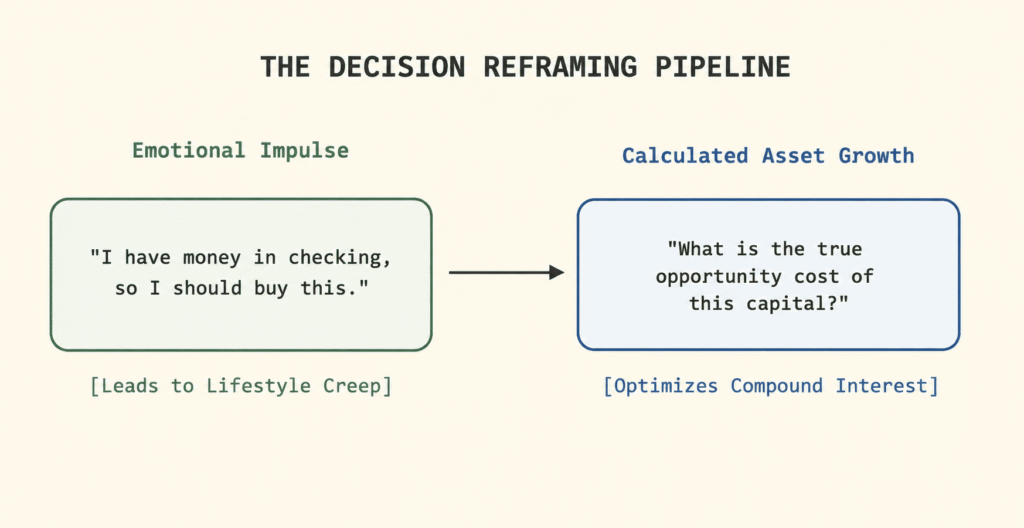

The secret to making smart banking decisions is to step away from emotional impulses and to use a structured, data-driven framework.

Every spending or saving decision has a ripple effect on your overall net worth, so you need to evaluate it deliberately.

To incorporate Advanced Banking Strategies into your daily routine, apply these three essential filters to all major financial decisions:

- The Opportunity Cost Analysis: Think about it: a dollar you spend on an asset that’s losing value fast is a dollar you can’t put to work earning interest in a high-yield environment.

- The Operational Cost Test: Do not just look at the price tag of a financial product or service. Look out for the structural fees, structural minimum balances or maintenance penalties that are built into the contract.

- The Time-Horizon Test: Match your liquid capital with its real operating horizon. Keep accessible short-term emergency money, and put your long-term wealth into investment vehicles that compound well.

Mindset Changes: Distinguishing Needs from Wants in Personal Finance

How you account for your outbound cash is what determines the difference between financial stability and a cycle of debt. The ultimate structural defense against lifestyle inflation is mastering the concept of needs vs wants in personal finance.

The infographic above gives you a clean plan to audit your cash flow using the 50/30/20 allocation rule:

1. Needs (50%):

These are your survival costs that cannot be compromised. These are things like your rent or mortgage, utilities, minimum debt service obligations, health insurance, and basic groceries.

2. The Wants (30%):

These are the lifestyle upgrades you want. This includes things like eating out, entertainment subscriptions, luxury travel, and non-essential clothing.

3. The Savings (20%).

This is your primary wealth-building engine. It is the principal set aside for rainy-day funds, high-return retirement accounts, and investment goals.

By maintaining a tight rein on this balance, you ensure that your lifestyle choices do not come in the way of your long-term financial growth.

To learn more about which strategy is suitable for you, needs, wants, and saving, take a consultation from a specialist Finance Nest Consultation agency. The agency owns a certified and seasoned consultant who can offer you the right path.

Balancing Act: Defining Your Needs vs. Wants

To understand personal finance, you must distinguish between essential survival costs and lifestyle choices. Misclassified costs are the main cause of budget overruns.

1. Your Absolute Needs (50% allocation):

These are the non-negotiable obligations needed to survive and be legally or professionally compliant.

Examples: Basic necessities like rent or mortgage, groceries (not eating out), utilities (electricity, water, internet), health insurance, public transit or basic car expenses, and minimum debt payments.

2. Your Wants (30%)

Although optional, these choices improve your quality of life and comfort.

Examples: Such as streaming services, takeout, gym memberships, vacations, hobbies, concert tickets, and designer clothes.

3. Future Savings (20% Allocation):

This is your defensive capital for wealth creation, long-term security, and financial peace of mind.

Examples: Monthly emergency fund contributions in a high-yield savings account, automatic retirement account transfers, additional principal payments to speed debt repayment, and automatic investment account contributions for long-term growth.

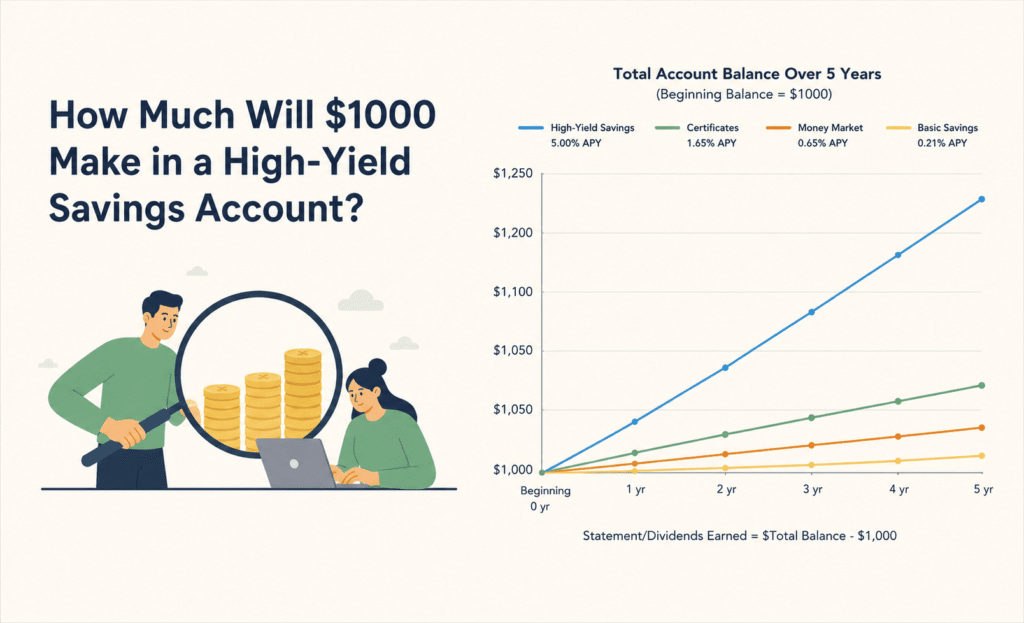

Top High-Yield Savings Accounts for Long-Term Goals

It’s an expensive error to hold your main emergency cushion in a standard brick-and-mortar checking or savings account.

These days, standard banks pay a national average savings yield of about 0.46% Annual Percentage Yield (APY). Which means, inflation is actively eating away at your real purchasing power every single day.

Your money can do the heavy lifting for you by moving your capital into the best high-yield savings accounts for long-term goals.

Best High-Yield Savings Accounts

- Forbright Bank Growth Savings – 4.15% APY, but you have to maintain a minimum balance to earn APY. If you’re like me and prefer HYSAs with eco-friendly investment missions, all the better.

- CIT Bank Platinum Savings: Earns 4.10% APY. You can earn the most money by using the CITBOOST promo code for new deposits.

- Bask Bank Interest Savings 4.10% APY. There are no monthly fees, and there is a $0 minimum to earn the stated yield.

The Pros and Cons of High-Yield Savings Accounts

Before you decide to open an account, consider the pros and cons of high-yield savings accounts.

Pros of HYSAs

- Benefit from higher interest rates than a regular savings account

- You can access your money easily without early withdrawal fees, like with a CD

- Most HYSAs provide deposit insurance of $250,000 per person, per ownership category, for accounts you hold at the financial institution, protecting you if the financial institution fails.

Cons of HYSA

- APY is subject to change at any time

- Using an online-only HYSA may make it harder to deposit and withdraw cash

- Might get you a lower return than if you invested or put it in a CD

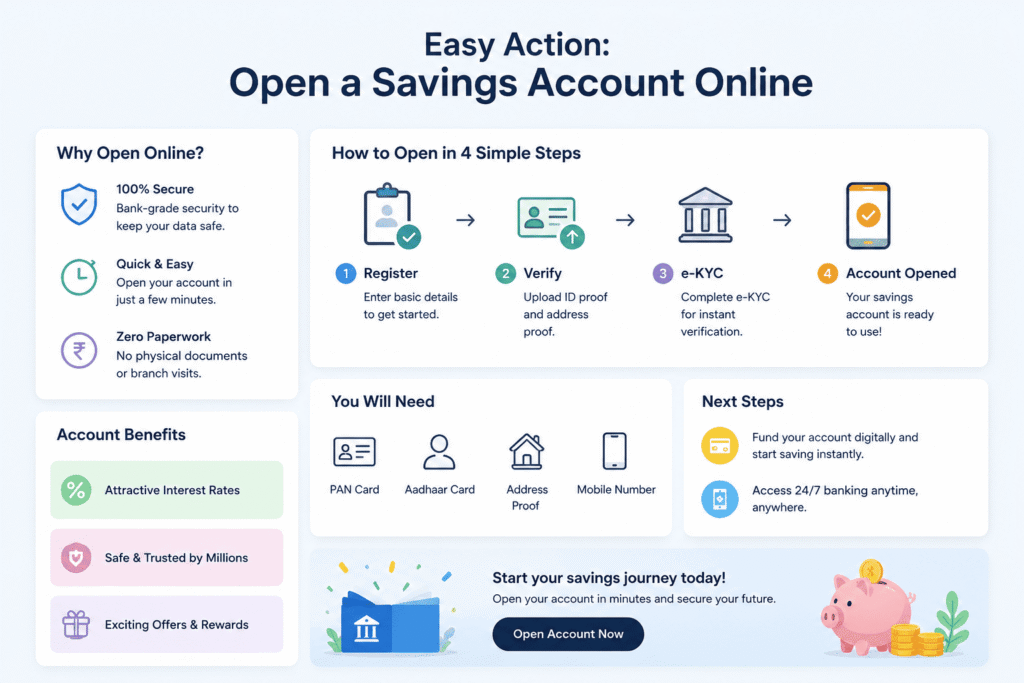

Easy Action: Open a Savings Account Online

Gone are the days of taking time away from work, driving to a local branch, standing in long lines, and signing thick stacks of paper.

You can open a savings account from the comfort of your couch in under ten minutes.

For a fast and efficient way to get a premium high-yield account, please follow these simple steps:

- Compare Current Yields: Use trusted financial comparison websites to find premier online banking institutions that provide the best APY rewards with no monthly administrative maintenance fees.

- Gather Digital Documentation: Have your government-issued ID, Social Security Number (SSN), and key bank routing numbers on hand to pass the secure identity verification check.

- Fill in the digital application, create your security credentials, and connect your first external account through the bank’s encrypted platform, and fill in the automated form.

- Fund the Account Now: Electronically transfer funds (ACH) to deposit your first savings balance and set up your automatic monthly savings plan.

Conclusion: Take Charge of Your Financial Legacy

Your smart banking decisions and habits dictate the path of your financial journey.

By taking your money out of a low-yield traditional bank and putting it into an automated digital high-yield savings vehicle, you stop losing money to inflation and start building real wealth

See every dollar as a purposeful asset. And hence unnecessary bank fees. Leverage modern online banking tools to secure your long-term financial freedom.

FAQs

- Are online banks safe and protected by federal insurance?Yes, they are completely safe, as long as they are guaranteed by the federal government. The best-in-class digital banking platforms are fully insured with the Federal Deposit Insurance Corporation (FDIC) for traditional banks or the National Credit Union Administration (NCUA) for credit unions. This insurance covers your personal deposits up to $250,000 per depositor, per institution, meaning your money is safe if the bank goes under.

- What is the difference between a high-yield savings account and a CD?The key is flexibility and access. A high-yield savings account offers variable interest rates. It also lets you withdraw your cash at any time you need it, which makes it perfect for emergency funds. A Certificate of Deposit (CD) is a way to put your money away in a locked box for a certain amount of time, such as 12 or 24 months, and receive a fixed interest rate in return. There is usually a penalty fee for early withdrawal from a CD.

- Do the interest rates on online high-yield savings accounts change?They do. Yes. High-yield savings accounts usually have variable interest rates, which means that their yields can go up or down depending on macroeconomic benchmarks set by the Federal Reserve. When the Fed adjusts its target rate, online banks will usually move in lockstep with their account yields.

- How long does it take to move money from my online bank back into my regular checking account?Electronic transfers (ACH transfers) between an online bank and a traditional local bank generally take 1 to 3 business days to clear. If you want faster access to your cash, look for online institutions that offer a dedicated ATM debit card or instant peer-to-peer payment transfers.

- Do I need to make a large initial deposit to open an online savings account?Certainly not. The majority of the best online financial platforms do not have a minimum initial deposit and do not charge monthly maintenance fees. This friendly arrangement enables you to deposit whatever you have available in your account and gradually build your wealth with consistent monthly contributions.